Power Of Attorney Format For Authorised Signatory For Income Tax

Loan Clearance Letter Sample Five Ingenious Ways You Can Do With Loan Clearance Letter Sampl In 2020 Lettering Loan Letter Sample

Free Authorization To Release Information Form Power Of Attorney Form Real Estate Forms Lettering

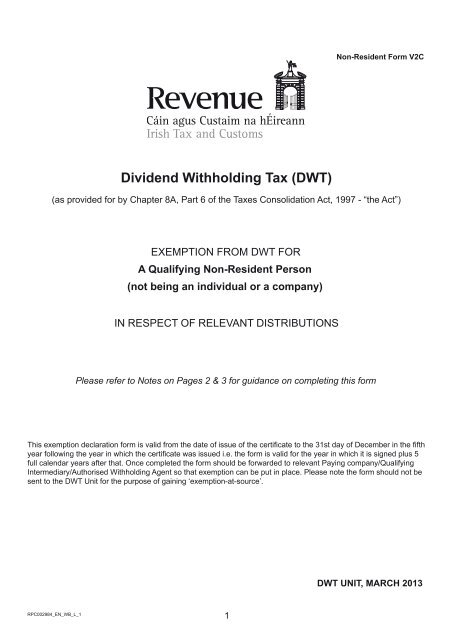

Form V2c Revenue Commissioners

Https Www Ubs Com Au En Asset Management Funds And Prices Forms Jcr Content Mainpar Toplevelgrid Col1 Linklist 702988172 Link 1223452651 0074030770 File Bgluay9wyxrops9jb250zw50l2rhbs9zdgf0awmvyxnzzxrfbwfuywdlbwvudc9hdxn0cmfsawevcgrzl3rhec1pbmzvcm1hdglvbi1mb3jtlnbkzg Tax Information Form Pdf

Edgar Filing Documents For 0000018498 19 000051

Http Media Corporate Ir Net Media Files Irol 75 75146 Qualifying 20non Resident 20company 20form 20v2b Pdf

The trustee executor or other fiduciary responsible for filing the form 1041 return.

Power of attorney format for authorised signatory for income tax.

Https Www Crs Hsbc Com Media Crs Pdfs Russia Cmb Crs E Entities Self Cert Form Pdf

Https Www Crs Hsbc Com Media Crs Pdfs New Zealand Cmb Crs E Entities Self Cert Form Nz Pdf

Spa

Indiafilings Indiafilings Twitter Republic Day Happy

General Power Of Attorney Template Get Free Sample

Https Www Crs Hsbc Com Media Crs Pdfs Qatar Rbwm Crs E Entities Self Cert Form Qatar Pdf

Https Www Crs Hsbc Com Media Crs Pdfs Channel Islands Crs I Self Cert Form 11 May 16 Ciiom Pdf

Https Cda Au Computershare Com Content 2cbd3c35 2278 4abb 8e66 Cb791e025323

Power Of Attorney Format

Https Www Crs Hsbc Com En Cmb Media E17e7d8aa9d9420689e6ae2b6450bcae Ashx

Https Www Bankfab Com Media Fabgroup Home About Fab Corporate Governance Compliance Documents Compliance Documents Pdfs Oecdcrsandusfactaselfcertificationformforentities Pdf View 1

Ex101schuhamendmentandre

Https Www Ecabank Com Home Assets Files Hcc Thumbs Individual Self Cert Form 20editable Pdf

Free 6 Sample Tax Invoice Forms In Excel Pdf

Http Www Taxfind Ie Binarydocument Pdfs Http Www Revenue Ie En Practitioner Tech Guide Joelife03 Pdf Pdf

Exhibit102sharepurchasea

Https Www Eastspring Com Docs Librariesprovider18 Application Forms Fatca Crs Individual Pdf Sfvrsn C2cd777f 2

Https Www Credit Suisse Com Media Assets Corporate Docs About Us Responsibility Banking Aic Aei Entities Oecd Ag En Pdf

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcsvnpo90lhcfm A12vxlsditqigddkqzmeyooyhdatpepbyegcn Usqp Cau

Https Craigsip Com Media Craigsip Files Other Tax Residency Self Certification Entities Pdf La En Hash 34785c5969fd4199e01d1e5600dedf01449c0b5a

Https Cda Computershare Com Content 4f57aa01 7108 4716 B51b 6334a33657d9

Https Www Dtcc Com Media Files Pdf 2020 7 6 13582 20 Pdf

Http Office Incometaxindia Gov In Lucknow Lists Tenders Attachments 6 Hiring 20premises 2 Pdf

Image Result For Gst Format Delivery Challan Invoicing Debit Banking Institution

Source : pinterest.com